Growth hits 0.5% in Q3 — a nation shrugs

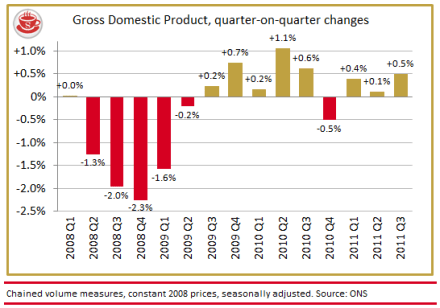

The growth number for the third quarter of this year is out, and it’s a little bit better than expected: 0.5 per cent. Many economists were saying that we’d have to hit around 0.4 per cent to recoup the growth lost to the Royal Wedding and Japanese Tsunami in Q2, so we’ve managed that. But, that aside, this is not the time for party poppers and champagne corks. It may not be Econopocalypse, but it’s not Mega Growth either. We are still living in a bleak, borderline stagflationary environment. Besides, I still reckon that we oughtn’t get especially worked up about these quarterly figures anyway. For starters, the obsession over